Sales of thin-film transistor (TFT) LCD manufacturing equipment are expected to surge 58 percent to reach a value of $13 billion in 2008, according to the “Quarterly TFT LCD Supply/Demand and Capital Spending Report,” which was published in June 2008 by DisplaySearch of Austin, Texas. The report also provides a broader prospective of the flat panel display industry, through discussion of color filter, module, plasma display panel (PDP) and organic LED fabrication activity.

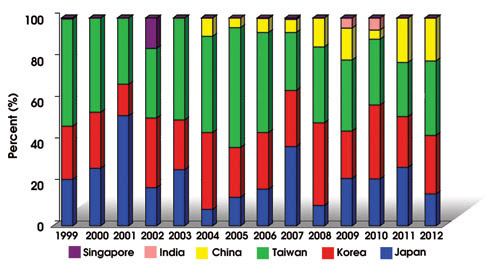

Percentages of second quarter 2008 thin-film transistor equipment spending by region are listed for the years 1999 to 2007 and forecast for 2008 through 2012. It is assumed that there is 100 percent revenue on shipments. Courtesy of DisplaySearch.

Charles Annis, vice president of manufacturing for DisplaySearch, provided some background information on the recent rebound. He noted that, in 2004, spending jumped to $13.3 billion, driven by a large number of investments, such as in the Generation 5 factories in Taiwan and China and in the Generation 6 and 7 lines. In 2005, spending was down as the industry reacted to 2004 and, in 2006, total equipment expenditures increased by 20 percent to an estimated $12.6 billion as the race took off to gain share in the rapidly expanding LCD television market.

Annis said that excessive investments from 2004 into 2006 led to an oversupply of panels, driving pricing down faster than costs could fall and causing industry-wide losses in 2006 and into the first quarter of 2007. Panel makers consequently delayed expansion plans, bringing down 2007 spending by 34 percent, to $8.2 billion. At the same time, however, demand for panels soared as a result of low prices, causing shortages in 2007 and now driving the wave of capacity expansion in 2008.

Industry forecasts

According to Annis, although 2009 was forecast to be a strong year for TFT LCD equipment spending – Sharp Corp. of Osaka, Japan, is moving ahead with Generation 10 plans, IPS Alpha Technology Ltd. of Chiba, Japan, is building a new Generation 8 facility, and Taiwanese, Korean and Chinese manufacturers plan to expand their LCD capacity – the slowdown in the world economy, weaker-than-expected demand, and rapid LCD module price decline in July and August 2008 may result in delays in some of the Taiwanese and Chinese fabrication expansions. Analysts now expect that 2009 spending could be down, Annis said, although it’s not expected to approach the 2007 lows.

The report indicates that TFT LCD array capacity is expected to rise at a compound annual growth rate of 35 percent, from 4.5 million square meters in 2000 to more than 235 million in 2013. Color filter capacity is expected to expand from 5.3 million square meters in 2000 to more than 253 million in 2013. It also notes that Panasonic Corp. (formerly Matsushita Electric Industrial Co. Ltd.) of Osaka is planning a 16-up 42-in.-equivalent PDP fabrication facility, and that some Chinese companies are building new facilities for these displays. Among them, Nanjing Huaxian Technologies plans to implement a new shadow-mask-based PDP technology that avoids the barrier rib process and reduces costs.

Analysis shows that the top five LCD manufacturers would continue to invest at the highest rates, increasing their total share of capacity from 80.5 percent in first quarter 2008 to 82.5 percent in 2010.

Among other predictions, TV areal demand will grow from 38 million square meters in 2008 to more than 68 million in 2012. It is expected that 120 million LCD television modules will be shipped in 2008, and that this figure will increase to 200 million in 2012.

Also, in 2008, it is expected that Korea, Taiwan, China and Japan will account for 40, 37, 14 and 10 percent, respectively, of the total TFT LCD equipment spending, and that the latter two countries will increase their spending in this area during the forecast period.